Florida Home Insurance: Construction Types, Roof Shapes, Fire Protection, Discounts & Every Factor That Impacts Your Rate

Florida home insurance pricing isn’t random — it’s engineering, risk modeling, and decades of hurricane and claims data. Two homes on the same street can have completely different premiums because carriers evaluate dozens of factors behind the scenes.

This guide breaks down every major rating factor in Florida, including:

- Construction type: wood frame vs. masonry (CBS)

- Roof shape: hip, gable, flat

- Roof material: shingle, metal, tile

- Fire protection: hydrant distance & fire station proximity

- Home age: newer vs. older homes

- Location: coastal vs. inland, wind zones

- Realistic discounts: what actually moves the needle

- Other underwriting factors: claims, updates, pools, dogs, rentals

🧱1. Construction Type: Wood Frame vs. Masonry (CBS)

In Florida, carriers classify homes primarily as either masonry (concrete block) or wood frame. That single difference can dramatically change your premium.

Masonry (CBS – Concrete Block Structure)

- Concrete block exterior walls

- Steel reinforcement inside the block

- Excellent wind resistance

- Excellent fire resistance

- Lower likelihood of total loss

Why masonry is usually cheaper to insure

- Concrete doesn’t burn — fire spreads slower and is easier to contain.

- Concrete doesn’t twist in wind — better performance in hurricanes.

- Lower claim severity — damage is often repairable instead of total loss.

- Lower reinsurance cost — carriers pay less to reinsure masonry portfolios.

Typical impact: masonry homes often cost 15–35% less to insure than comparable wood frame homes.

Wood Frame Construction

- Wood studs and sheathing

- Lighter, more flexible structure

- More vulnerable to fire

- More vulnerable to wind and racking

Why frame homes usually cost more

- Fire spreads rapidly — wood ignites and burns quickly.

- Wind can rack or shift the structure — more structural damage in storms.

- Higher claim severity — more total losses, higher payouts.

- More expensive to reinsure — reinsurers charge more for frame exposure in hurricane states.

Typical impact: frame homes can cost 30–60% more than masonry in coastal or high‑risk counties.

| Factor | Masonry (CBS) | Wood Frame |

|---|---|---|

| Fire resistance | High – concrete doesn’t burn | Low – wood ignites and spreads fire |

| Wind resistance | Strong, rigid walls | More flexible, more structural movement |

| Typical premium | Lower | Higher |

| Claim severity | Often repairable | Higher chance of total loss |

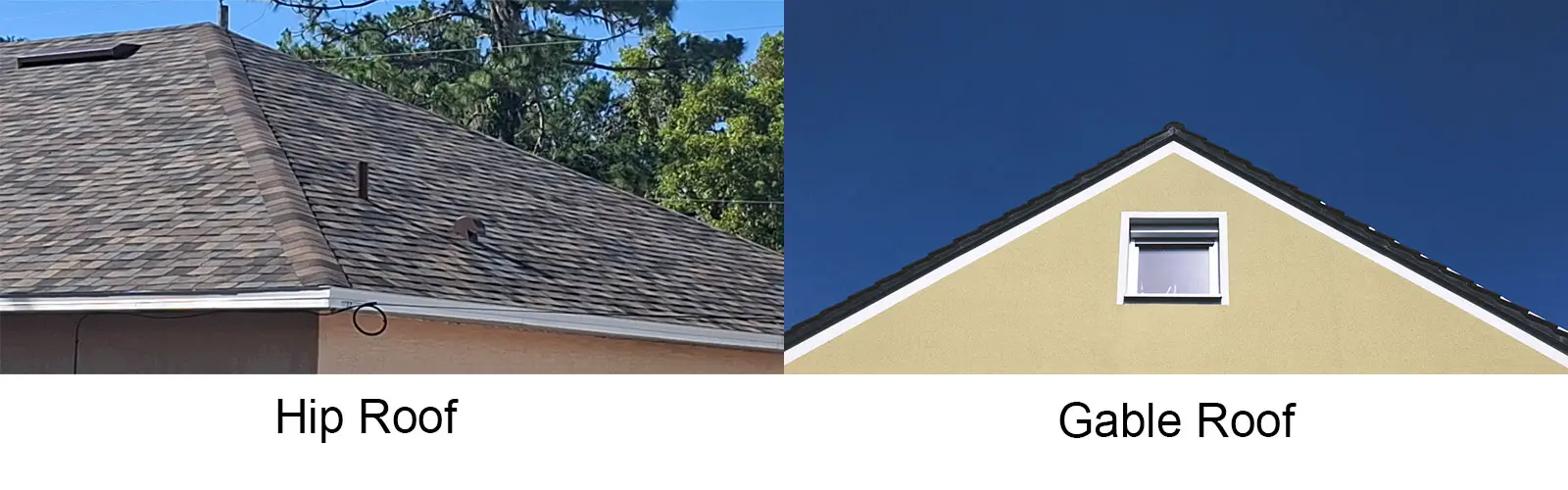

🏠2. Roof Shape: Hip vs. Gable vs. Flat

Roof geometry is one of the biggest rating factors in Florida. Carriers care about how wind hits your roof and how likely it is to fail.

Hip Roof (Usually the Lowest Cost)

What it is: a roof that slopes down on all four sides.

Why hip roofs are cheaper

- Wind flows over them smoothly — less uplift pressure.

- Fewer failure points — no large vertical gable ends to catch wind.

- Best hurricane performance — historically fewer catastrophic failures.

Typical impact: a hip roof can reduce premiums by 10–25%.

Gable Roof (Moderate Cost)

What it is: two sloped sides with a vertical wall at each end.

Why gable roofs cost more

- Gable ends catch wind like a sail — more uplift and pressure.

- More structural bracing required — if not properly braced, gable ends can fail.

Flat Roof (Highest Cost)

What it is: flat or very low‑slope roof.

Why flat roofs are expensive

- Water pooling increases leak risk.

- Poor drainage can cause damage.

- Shorter lifespan in Florida’s climate.

Typical impact: flat roofs can increase premiums by 20–40%. (primarily due to limited carrier acceptance of flat roof shaped homes. Otherwise rate may be closer in line to a gable roof house).

🛠️3. Roof Material: Shingle, Metal, Tile

Asphalt Shingle

- Most common roof type in Florida.

- Typical lifespan: 15–25 years.

- Most vulnerable to wind uplift.

Metal Roof

- Excellent wind resistance.

- Typical lifespan: 40–70 years.

- Excellent energy efficiency to lower utility bills

Tile Roof

- Strong wind resistance when properly attached.

- Heavy and expensive to repair.

- Attachment method matters for rating.

🔥4. Fire Protection: Hydrant Distance & Fire Station Proximity

Fire protection class is a major rating factor, especially for frame homes. Carriers look at how quickly the fire department can reach you and how much water they have available.

Key Fire Protection Factors

- Distance to nearest fire hydrant

- Distance to nearest fire station

- Career vs. volunteer station

- ISO fire protection score

Typical distance thresholds

- 0–1,000 feet: best rate

- 1,001–2,500 feet: moderate

- 2,500+ feet or no hydrant: high risk

Typical impact: homes far from hydrants or stations can pay 20–50% more.

🗓️5. Why Newer Homes Often Cost More Than Older Homes

Newer homes often have higher premiums because their replacement cost is higher — modern materials, labor, and finishes cost more.

Why newer homes cost more

- Higher replacement cost

- Larger square footage

- Higher Coverage A limits

But newer homes get big credits

- New construction discount

- New roof credit

- Modern building codes

- Updated systems

🏚️6. Why Older Homes Sometimes Cost Less — and Sometimes Much More

Older homes that rate well

- Newer roof

- Updated plumbing

- Updated electrical

- Wind mitigation documentation

Older homes that rate poorly

- Old roof

- Outdated plumbing

- Obsolete electrical panels

- No wind mitigation

📍7. Location: Why Your ZIP Code and County Matter

Location is one of the biggest drivers of home insurance cost in Florida.

Examples of location‑driven differences

- Coastal counties = highest wind & litigation risk

- Inland counties = lower wind risk

- Barrier islands = highest premiums

Two identical homes — one inland, one near the coast — can differ by 50–200% in premium.

💸8. Realistic Discounts Florida Homeowners Can Get

High‑impact discounts

- Wind mitigation inspection

- Hip roof

- Newer roof

- Centrally monitored alarms

- Sprinkler system

- Gated community

- Military/veteran

- Electronic policy delivery

Smaller discounts

- Smart home devices

- Water leak sensors

- HOA membership

📋9. Other Underwriting Factors Carriers Use

Home updates

- Roof

- Plumbing

- Electrical

- HVAC

Claims history

- Water damage

- Roof claims

- Liability claims

Liability‑related factors

- Dog breeds

- Swimming pools

- Trampolines

Occupancy and use

- Primary vs. seasonal

- Short‑term rental

- Tenant‑occupied

📊10. Summary: Why Two Homes Can Have Completely Different Premiums

| Factor | Lower Cost Scenario | Higher Cost Scenario |

|---|---|---|

| Construction | Masonry (CBS) | Wood frame |

| Roof shape | Hip roof | Gable or flat roof |

| Roof material | Newer metal or architectural shingle | Older shingle or aging flat roof |

| Fire protection | Hydrant nearby | No hydrant |

| Home age | Newer home | Older home with no updates |

| Location | Inland | Coastal |

| Discounts | Wind mitigation, alarms | No mitigation |

| Claims history | Clean | Multiple prior claims |

Frequently Asked Questions

Is a masonry home always cheaper to insure?

Not always, but in Florida it usually is. Masonry performs better in wind and fire, which lowers claim severity.

How much can a wind mitigation inspection save me?

It depends on the credits shown on your wind mitigation inspection. It’s often the single biggest discount available in Florida.

Why does my neighbor pay less?

Even small differences — roof age, roof shape, construction, hydrant distance — can dramatically change premiums.

Do gated communities lower insurance?

Yes, many carriers offer a small discount for gated or secured communities.

Why does roof age matter so much?

Roofs are one of the most common sources of claims in Florida. Older roofs are more vulnerable to wind and water damage.

Request a Homeowners Insurance Quote

If you’d like help comparing your builder’s quote, understanding coverage options, or getting a fast binder for your lender, I’m here to make the process simple for your next real estate closing.

Learning Center Navigation

Related Florida Insurance Pages

Get a Florida Home Insurance Quote

No matter where you live in Florida, I can help you compare rates from multiple carriers and find the best homeowners insurance options for your property.

Ready to Get Started?

I’m here to help you find the right coverage at the right price — with no pressure and no confusion.